Warren Buffett’s seemingly most popular quote “Price is what You pay and Value is what You get” doesn’t seem more destroyed or intrigues the patron more, when one pays ~Rs300 / USD 4.5 for a 100 gms box of popcorn at an Indian multiplex, whereas in India 700 million people earn less than Rs 100 per day or say ~USD1.4 / day

But this piece isn’t about the Indian Economy, its about the market darling – PVR Cinemas.

The purpose of this piece is to inform the gullible minority shareholder that while all the institutions are dumpin the favourite PVR stock, You are being made the muppets and when the music stops, you will have nowhere to run. Its pertinent to mention that the shareholding of people with less than 20,000 shares has shot up from 3.5 – 10.5% in a matter of just 9 months.

PVR generates an EBITDA of Rs 60 per patron / movie watcher

Sale of F&B is Rs. 948crs or ~ 28.8% of total sales and 55% of Movie Sales Revenue or Rs. 93/patron.

Cost of F&B is 8% of sales thus 72.5% Profit Margin on Popcorn or say Rs. 67/Patron comes from F&B

Which means EBITDA Loss of Rs. 7/patron is generated by (Sale of tickets + Advertisement Income + Convenience Fees + Other Operating Income) the core business.

SO ITS SAFE TO ASSUME THAT PVR IS JUST A POPCORN AND A NACHOS COMPANY

I feel sorry for the shareholders of the company that places its QIP at Rs 1719 and within a few months has to come up with a rights issue at Rs 784 because the ever burgeoning debt, is unmanageable, future is uncertain and probably the promoters have to be paid arrears of their handsome increments even while the wealth of minority shareholders is being blatantly destroyed – some by pandemic – some by the promoters.

Here are the statistics

As per the management, in a recent concall in May, the breakeven of PVR is at at 20% occupancy and Average Occ that PVR enjoyed is 35% in precovid times (And achieved an 18% EBIDTA and 0.8% PAT margin), One question that comes to mind is – if capacity utilisation in the best of the times is 35% generating such abysmally low PAT, what effect will a lower occupancy have on the P&L and the Balance Sheet

And the EBIDTA sucks because the promoters who own a mere 18.79% of this company draw a cumulative salary (besides all other perks and privileges) of ~ 28 Crores that is slightly more than the PAT of the company. A back of the envelope calculation pegs the EPS for promoters and family at approx Rs 32 per share while its a paltry Rs 4.95 for other shareholders.

It’s a shame – more so in India – because stockmarkets are shallow, lack depth, and most shareholders have no access to genuine research on the basic and key metrics of the company, intention of the management, and self centricity of the promoters at the cost of minority shareholders.

PVR has been incurring ~ monthly expenses of 63 Cr (assuming 50% waiver on rent and CAM charges) so if this year is more or less a washout, it would have burnt approx. 750 Cr without any mentionable revenue in FY 2021) And that explains the short runway of the amount of Rs 300 Cr collected thru the rights (in Aug 2020) that might not have lasted beyond 5 months.

“The business is under a grave irreversible threat”

Ask a producer of a film and he/she is under permanent nervousness till one week after release of his movie – not knowing whether one would be able to recover costs, make profit or lose the skin.

The immense sense of freedom that most of the producers such as Ronnie Lahiri have found by releasing movies on OTT is heartening. Gulabo Sitabo was a great hit, made him the money and de-risked his investment. Top OTT players are happy to buy movies at a cost + basis, thereby de-risking the producers and the OTT players such as STAR, Amazon, Netflix have pockets tens of times deeper than the size of Indian film industry at ~13800 Cr (1.8 B USD) where the Bollywood is a mere ~1000-2000 Cr per annum

For the record Amazon and Flipkart burn a combined sum In excess of Rs 1,500 crores just during their Diwali sale alone.

OTT is really the future because a family can watch a movie in the convenience of ones Living room where the annual subscription of the most expensive platform is less than the cost of “just one” movie with the family at a multiplex. We haven’t yet discounted the pain of navigating the traffic, parking, lack of social distancing, risk in the AC (after Corona) world where the human psyche has got permanently mutated because of the present unexpected vicissitudes. The brilliant analysis by Seetharamanin The Ken sums up the dilemma and the zero sum game for the cinema halls.

No wonder that the sale of large TVs and projectors that cost as little as Rs 10 K on amazon has shot up in the recent times because of the newfound freedom by the movie buffs.

Low budget films, some of these dramatically awesome in content and direction, that cannot afford a big budget theatre release have found a new freedom and recognition and have been able to shed the risk bias of the patron because the incremental cost of watching this movie is almost nil for a family (if at all the same turns out to be a dud or below expectations). Not that the wounds inflicted on the populace by Salman Khans Tubelightor Aamir Khans Thugs of Hindostan can ever be healed. And on top of that the Rs 300 popcorns.

OTT reduces/almost-eliminates piracy and provides a reach to the most under provided sections of society where access might be a problem, but internet works at a good speed.

The demise of Cineworld with 9500 screens was a shock that had to down its shutters on almost 90% of its business due to the pandemic. And the hunger of retail shareholders to lap up the PVR stock seems unsatiable.

If this virus – that has permeated such degrees of fear in the society is here to stay for a foreseeable future then the future of multiplexes is in grave danger and that explains why the institutions or the big boys of the stock markets are strategically reducing their stake while holding the price at present levels and retail muppets (shareholders) are hungrily buying the stock to take the retail shareholding up from 3.55% in Dec 2019 to 10.32% by Sep 2020.

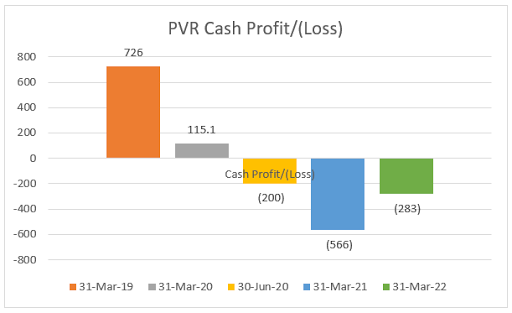

Unless another equity infusion takes place, The PVR debt will continue to burgeon, for many many years, to its peak of approx. 2100 Cr by Mar 2022.

Its loss might peak out at Rs 566 Cr by the end of this FY 2021

But the fact remains that – at the CMP of 1250 and FY 21 fwd PE of ‘maybe’ 1000, this is the most expensive stock on the planet beating Tesla dry and hollow and far ahead of its global peers such as AMC, Cineworld, Cinemark and Cineplex most of which have corrected by 60-90% while PVR is being distributed to the minority and gullible retail shareholders. (As there is absolutely no certainty on quantum and timing of full recovery, we have used Trailing numbers to benchmark globally. Also, a size discount is applied)

Going by these calculations and benchmarks, PVR (ceteris paribus) while deserving its rich valuations should slide down to under 400 when its performance, reasonable valuations meets to say hello to its eventual fate.

Minority shareholders singed by the narrative built around a stock always almost are left holding a rotten tomato.

Looking fwd to gain some confidence post this Virus, when I can again take my loving mom to get her favorite popcorns at PVR – in the meanwhile sell the family silver to check-in into PVR ‘only if’ there is no other show going on.

Ravi Sharma @caraviusharma ; https://www.linkedin.com/in/ca-ravi-u-sharma-65901b97/